📋 Highlights

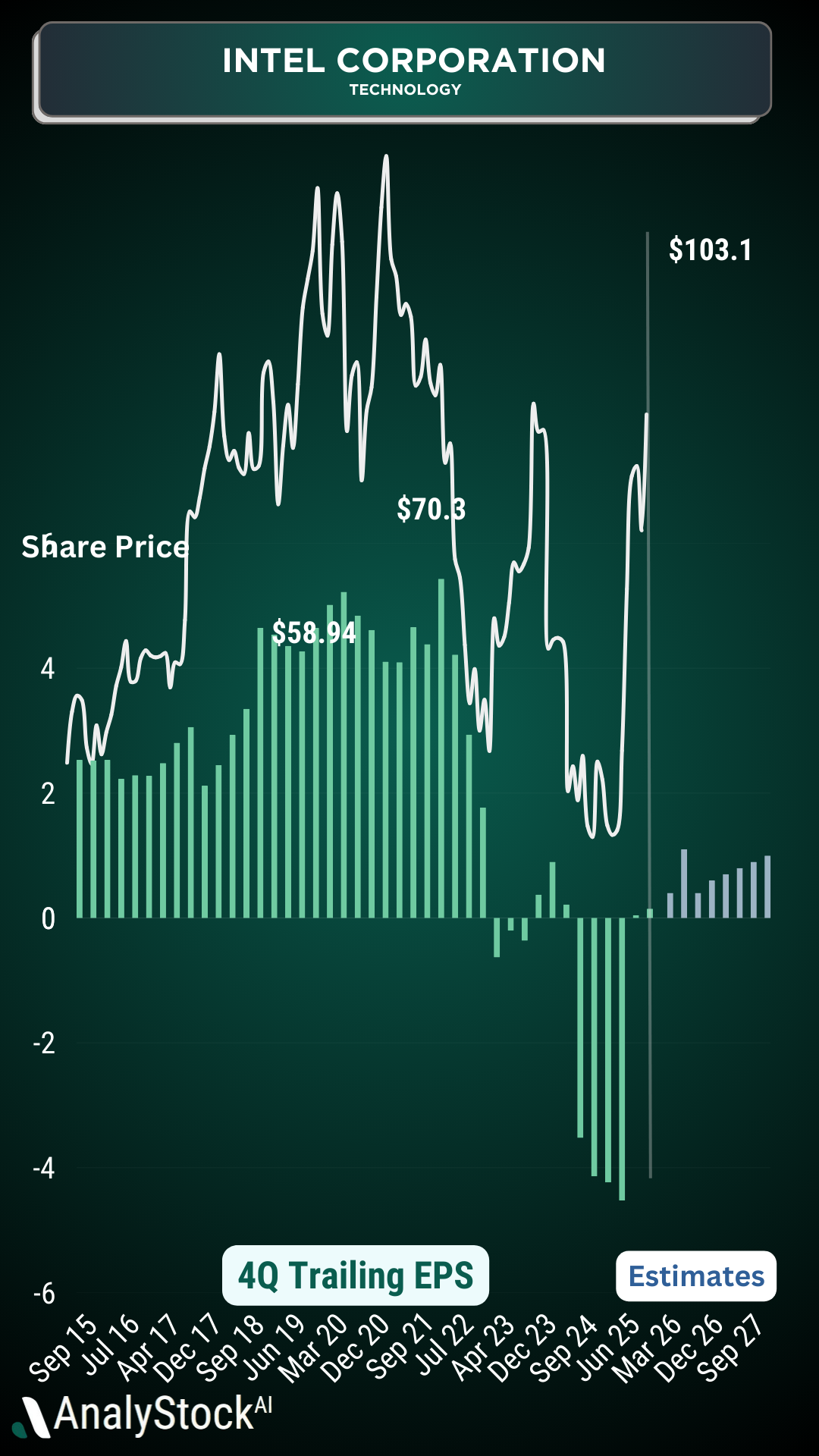

- Valuation Driven by Turnaround Potential, Not Current Fundamentals: Intel trades at 3.5× forward sales and 67× forward P/E, reflecting optimism around its foundry transformation rather than current profitability. Current valuations assume partial success in its strategic pivot but are still below peers like AMD and Nvidia.

- Strategic Investments Validate Foundry Ambitions: The U.S. government, Nvidia, and SoftBank have collectively invested $12.7B in Intel, signaling confidence in its 18A manufacturing node and future foundry capabilities. This funding is critical for capital-intensive projects and validates Intel’s path to competing with TSMC.

- Critical Catalyst: Panther Lake Launch in Q1 2026: The successful launch of Panther Lake processors on the 18A node in late January 2026 will be a pivotal test of Intel’s manufacturing progress. Strong performance and yield rates (>60%) could catalyze a re-rating of the stock toward growth multiples.

- Execution-Dependent Price Targets: Analysts project a base-case 12-month price range of $38–$48, with upside to $50–$60 if 18A proves competitive and external foundry wins accelerate. A bear case of $25–$30 hinges on yield failures or continued CPU share losses to AMD.

- Cautious Analyst Sentiment and Binary Outcomes: Wall Street remains split, with a "Hold" consensus and wide price target dispersion ($18–$52). The stock’s near-term direction hinges on operational proof points (e.g., 18A yields, margin expansion) rather than financial metrics, making it a high-risk, high-reward "execution story."